New National Poll Finds Consumers Still Want Financial Regulation

By Charlene Crowell –

A decade ago, the entire nation suffered through a financial crisis that led to the brink of a global financial collapse.

While Wall Street reckoned with its risky practices, America’s families suffered lost wealth of nearly $2 trillion, half of it coming from communities of color who were targeted for high-cost and unsustainable mortgages.

Now a new poll finds that even after the passage of a decade, consumers still support financial regulation and related enforcement. Moreover, when it comes to payday and car-title lending, consumer scorn has grown even stronger over the past year for these small-dollar, debt trap loans that come with triple-digit interest rates.

The 2018 poll, conducted by Lake Research Partners and Chesapeake Beach Consulting, found that among respondents more than 90% viewed regulation of financial services to be very important, registering support across partisan affiliations. Among Republicans, 85% supported regulation, compared to 92% of independents and 96% of Democrats.

The 2018 poll, conducted by Lake Research Partners and Chesapeake Beach Consulting, found that among respondents more than 90% viewed regulation of financial services to be very important, registering support across partisan affiliations. Among Republicans, 85% supported regulation, compared to 92% of independents and 96% of Democrats.

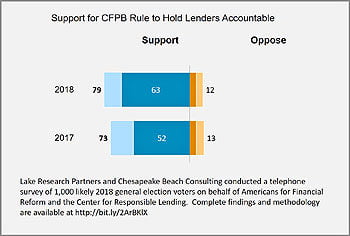

Further, the number of consumers supporting a rule to hold payday lenders accountable increased six percentage points in just the past year. Believing that payday lenders prey upon those who have the fewest financial resources—low-wage earners, working families, and elder Americans—79% of survey respondents want the Consumer Financial Protection Bureau (CFPB) to hold these predatory lenders accountable. A similar poll taken in 2017 tallied support of a CFPB payday rule at 73%.

Further, the number of consumers supporting a rule to hold payday lenders accountable increased six percentage points in just the past year. Believing that payday lenders prey upon those who have the fewest financial resources—low-wage earners, working families, and elder Americans—79% of survey respondents want the Consumer Financial Protection Bureau (CFPB) to hold these predatory lenders accountable. A similar poll taken in 2017 tallied support of a CFPB payday rule at 73%.

When asked about the lack of enforcement against abuses by payday lenders, 81% were concerned about CFPB’s inaction. Again, these strong responses crossed party lines: 77% of Republicans, 82% of independents, and 85% of Democrats.

The telephone survey of 1,000 likely 2018 general election voters occurred between June 28 and July 7, 2018, and has a margin of error of +/- 3.1%. The effort was jointly underwritten by Americans for Financial Reform (AFR) and the Center for Responsible Lending (CRL).

“Ten years after the financial crisis, the public knows what it wants,” noted Lisa Donner, AFR executive director. “But Wall Street and high-cost lenders are constantly pushing for deregulation and spending vast amounts of money to get it.”

The current federal deregulation trend can be traced to an executive order signed by President Donald Trump on January 20, 2017, and published in the Federal Register on February 3. The order directed all federal offices to repeal two existing regulations for every new one proposed. Also, for Fiscal Year 2017, no proposed regulation could include any costs. The Office of Management and Budget (OMB) was granted the sole authority to review and decide any requested written exceptions.

The OMB is led by Mick Mulvaney, who has simultaneously served as Acting Director of the Consumer Financial Protection Bureau since late 2017. So it is particularly noteworthy that 80% of survey respondents expressed concerns with three recent (CFPB) developments:

- Curbing the enforcement of fair lending rules;

- Ending enforcement of payday lending rules; and

- Restricting public access to the Bureau’s complaint database

- The 2018 survey results speak to the stark differences between CFPB today and its era before Mulvaney’s arrival.

As of July 2017, CFPB received approximately 1.3 million consumer complaints that were investigated and, in turn, led to enforcement actions that totaled $11.9 billion in restitution, forgiveness of consumer debt, and other enforcement. Because many of these were class action cases, an even larger number of consumers—29 million were helped.

Broad consumer contact and confidence was bolstered by visits to 41 cities where CFPB held either public town halls or field hearings on a given issue; 169 visits to military installations; and 63 appearances to testify before Congress.

“Before Mick Mulvaney’s tenure at the agency, the CFPB was a champion for working families—giving back billions of dollars in relief to consumers who were cheated by financial companies,” noted Mike Calhoun, CRL president. “Now, under the CFPB’s current leadership, payday lenders have preferred access because one of their own is leading the consumer bureau. We need to build on CFPB’s previous success, not block its progress of protecting consumers from abusive financial practices.”

Charlene Crowell is the communications deputy director with the Center for Responsible Lending. She can be reached at [email protected].